June 10, 2025

SUMMARY

As we approach summer and some of the initial hard data materializes, we revisit the landscape of US tariffs on Canada and take a brief look at how GDP and inflation (as well as the forecasts) have been faring.

TARIFFS: WHAT’S GOING ON HERE?

Much uncertainty persists as tariffs were frequently paused, pulled back altogether, or as we saw recently here in Canada, increased. On May 8, the UK was the first major country to strike a new trade deal with the US. On May 12, China and US came to a 90-day truce, going from as high as 145% to 30% tariffs on China, and a reduction from a high of 125% to 10% on US goods to China. The EU continues trade talks with the US as the 50% tariffs were delayed to July 9. However, reciprocal or 10% base tariffs will stay for almost all countries. Adding even more chaos to the mix, the U.S. Court of International Trade ruled that the use of the International Emergency Economic Power Act was an overreach of authority and ordered an immediate end to the collection of many of the tariffs (although this is of course being challenged and does not cover the industry specific tariffs on Canada). The U.S. may also use other powers to continue the imposition of tariffs (also see BMO, Trade War Shifts to the Courts).

CANADA TARIFFS

Canada was exempt from the ‘Liberation Day’ tariffs, but many other tariffs remain. This includes 25% on all goods that do not comply with CUSMA, 10% on energy related goods that do not comply with CUSMA, steel and aluminum tariffs which recently doubled to 50%, and 25% on non-US autos with carve outs for CUSMA content. Below we take a brief look at how the Canadian and Ontario economy have been weathering the storm so far.

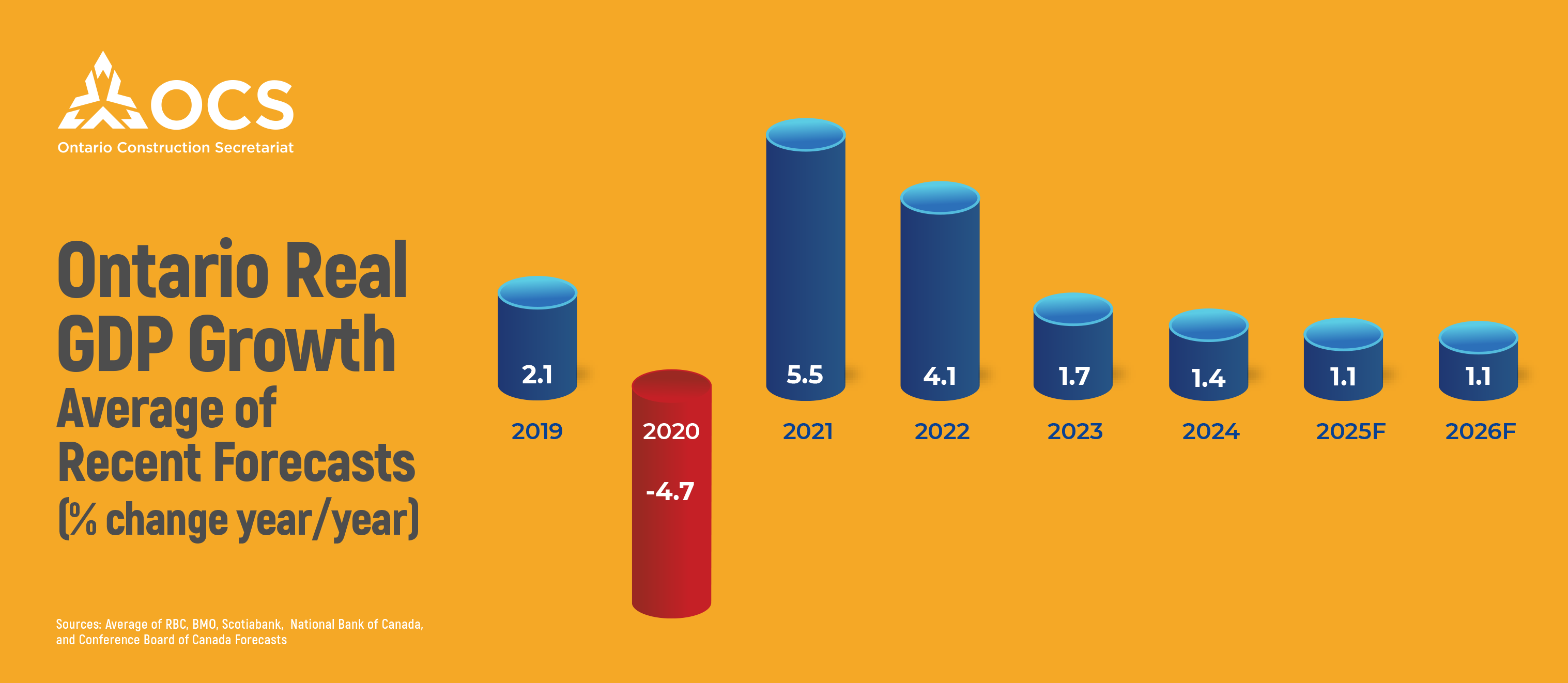

CANADIAN GDP FORECASTS

Canada’s GDP forecast saw sizable downward revisions since the threat of tariffs began to take shape. Pre-tariffs, growth was anticipated to return to around a healthy 2% in 2025, but since the imposition of tariffs this estimate was downgraded to a little over 1%, with some analysts predicting at least a quarter of contraction in 2025. Ontario forecasts have been a bit below the Canada average (due to higher exposure to the steel, aluminum, and auto tariffs) and will likely be revised down even more due to the doubling of steel and aluminum tariffs to 50%.

Despite the meek outlook, recent data delivered a welcome surprise as Canadian GDP grew by a solid 2.2%, slightly higher in Q4 2024 (2.1%). The preliminary estimates for April pointed to continued growth with a 0.1% monthly gain. Part of this resilience was due to stockpiling ahead of tariffs (particularly in machinery and investment) and boost in auto retail sales ahead of tariffs.

However, the Bank of Canada predicts that Q2 growth will be much weaker as the aforementioned pre-tariff activity fades out. The overall national unemployment rate now sits at 7% and major banks expect at peak of close to 8% over the course of the trade war. At the company level, Algoma Steel has already experienced layoffs, and Stellantis has seen several closures.

As the effects of the trade war continue to materialize, some of the impact will be cushioned by government initiatives. While a comprehensive federal plan has yet to be announced, the provincial government announced a plethora of initiatives (which we highlighted here) to help businesses affected by tariffs and support workers experiencing tariff-related layoffs.

As with the pandemic however, the construction industry continues marching forward. Infrastructure Ontario’s June Market Update detailed $30B worth of infrastructure projects in pre and active procurement and 19 more large scale projects in the planning stages.

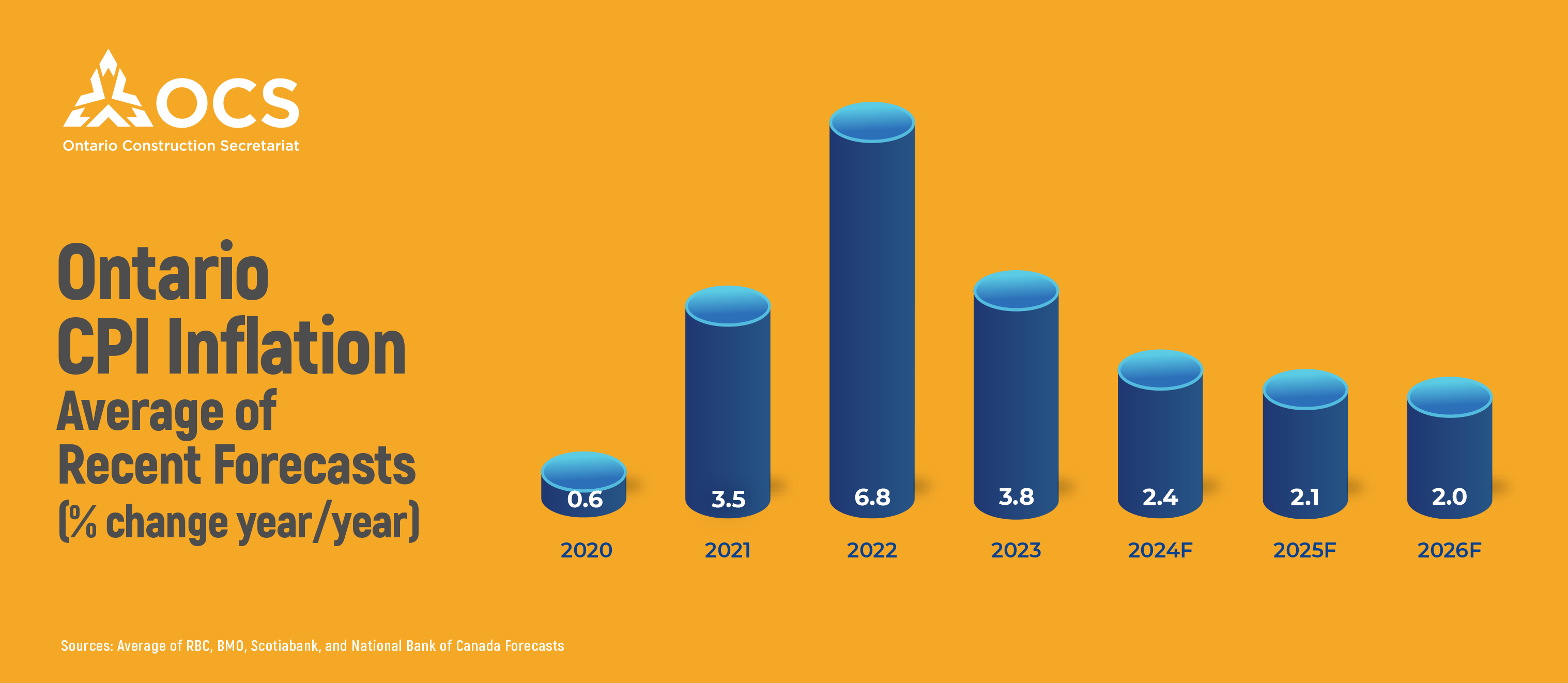

INFLATION FORECASTS

The latest headline inflation reading was 1.7% y/y in April, thanks to energy prices dropping steeply and the removal of the consumer carbon tax. Forecasted inflation is also projected to remain around 2% for the next few years. However, pressure remains from some areas including services, rent, and food, and the Bank of Canada’s preferred core inflation metrics, CPI-Trim and CPI-Median (see note), have crept up above 3%. Combining the firmer than expected GDP data and the rising underlying inflation, the Bank of Canada decided to hold interest rates at 2.75% in their June decision.

Note

CPI-Trim excludes items located at the tail end of the distribution of price changes, thus leaving out the most extreme prices changes (both the top and bottom 20 percent in a given month). CPI-Median follows the reading of the price change right in the middle of the distribution.

RECAP

Much has changed in the tariff landscape and the only certain thing is more uncertainty. Canada and Ontario have been spared the initially threated 25% tariffs on all goods, as well as the subsequent Liberation Day reciprocal tariffs, but 50% tariffs on steel and aluminum and 25% on autos remain a significant threat to the economy. As of now the data shows some resilience, as businesses and consumer scrambled to make purchases ahead of tariffs. Inflation, while creeping back up, remains largely in check with the fall in energy prices. However, the worst of the economic storm is yet to come, and we can expect the state of affairs in Q2 to be much weaker.

____________________________

FOR MORE INFORMATION, CONTACT:

Ali Ahmad

Research Analyst

Ontario Construction Secretariat (OCS)

180 Attwell Drive, Suite 360, Toronto, ON M9W 6A9

P 416.620.5210 ext. 222

aahmad@iciconstruction.com