Summary

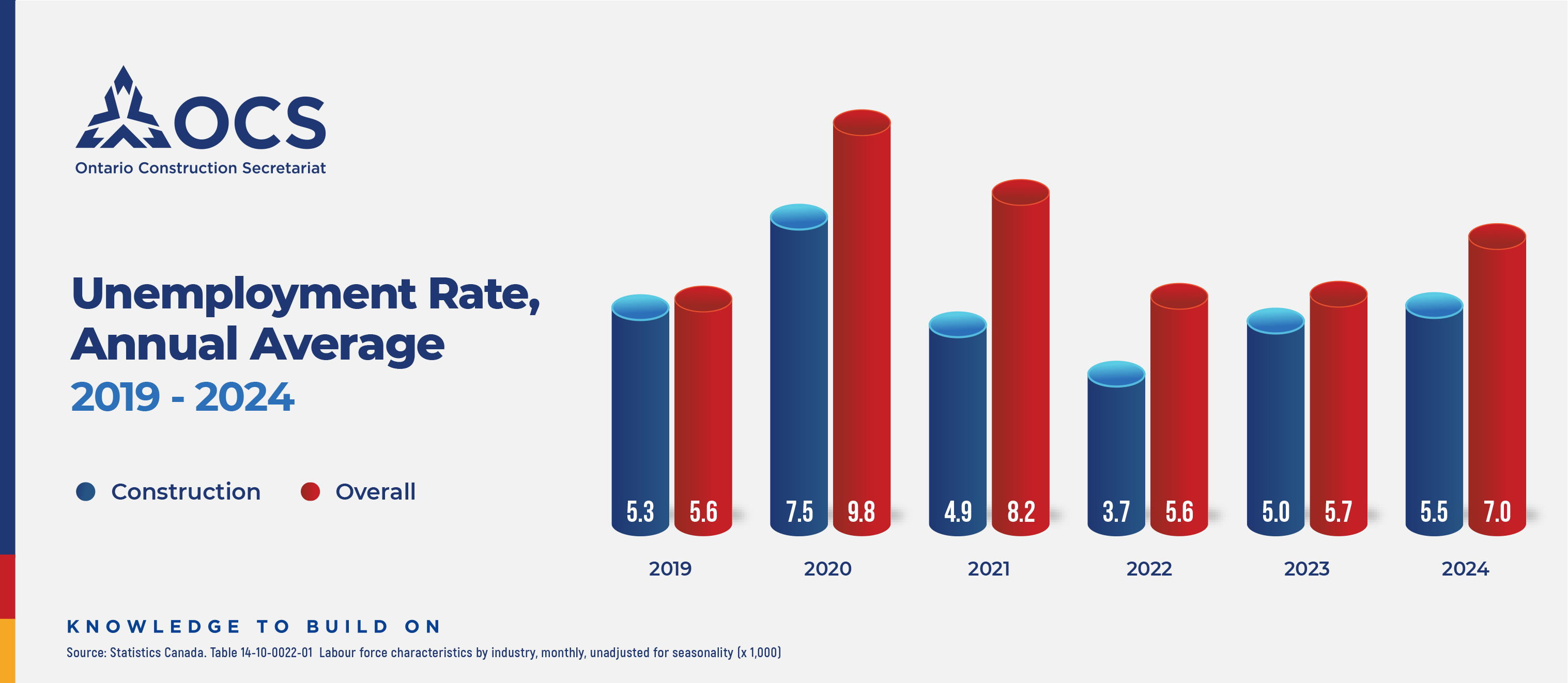

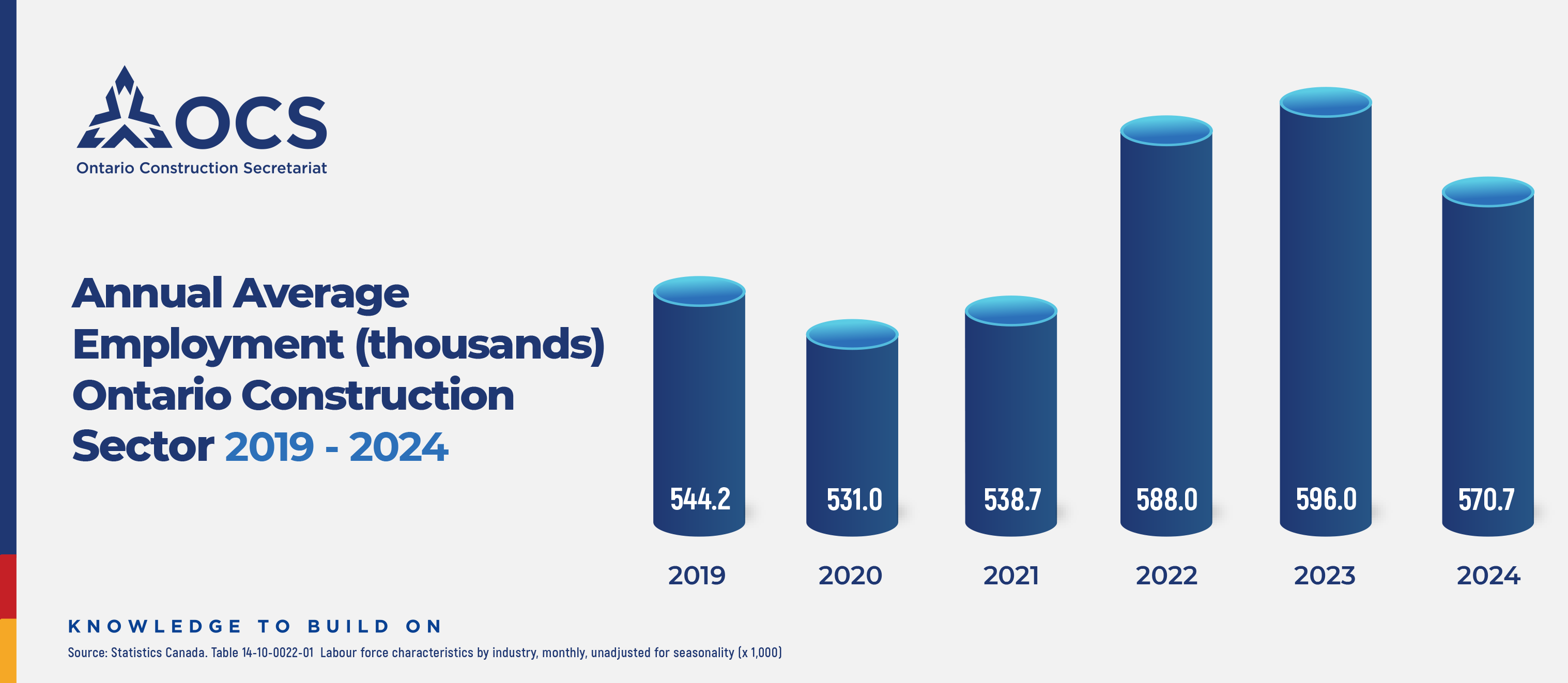

Employment in the Ontario construction industry soared over the last several years as the economy bounced back from the pandemic, breaking past previous record highs multiple times. In 2023, the annual average employment peaked at 596K workers with a labour force of 627.1K. Unemployment rates were also unusually low, averaging 3.7% in 2022. Despite the strong employment data on the surface, job vacancy rates revealed a strained labour market. These developments were fueled by the post-pandemic recovery and strong demand for construction. Conditions have moderated in 2024 as the economy slowed, with unemployment and job vacancy rates returning closer to pre-pandemic levels. However, an ongoing retirement wave is putting strain on the labour supply, while strong population growth – due to the federal government’s focus on immigration – is increasing construction demand. However, immigration also presents a golden opportunity to bring in more skilled trades workers. Diversifying the pool of labour with increased engagement from underrepresented groups also has the potential to address these labour market needs. While there remains room for improvement, the industry has made strides in the right direction, particularly as the number and share of women in construction improved.

Historically Low Unemployment Rates and Strong Employment in Ontario Construction

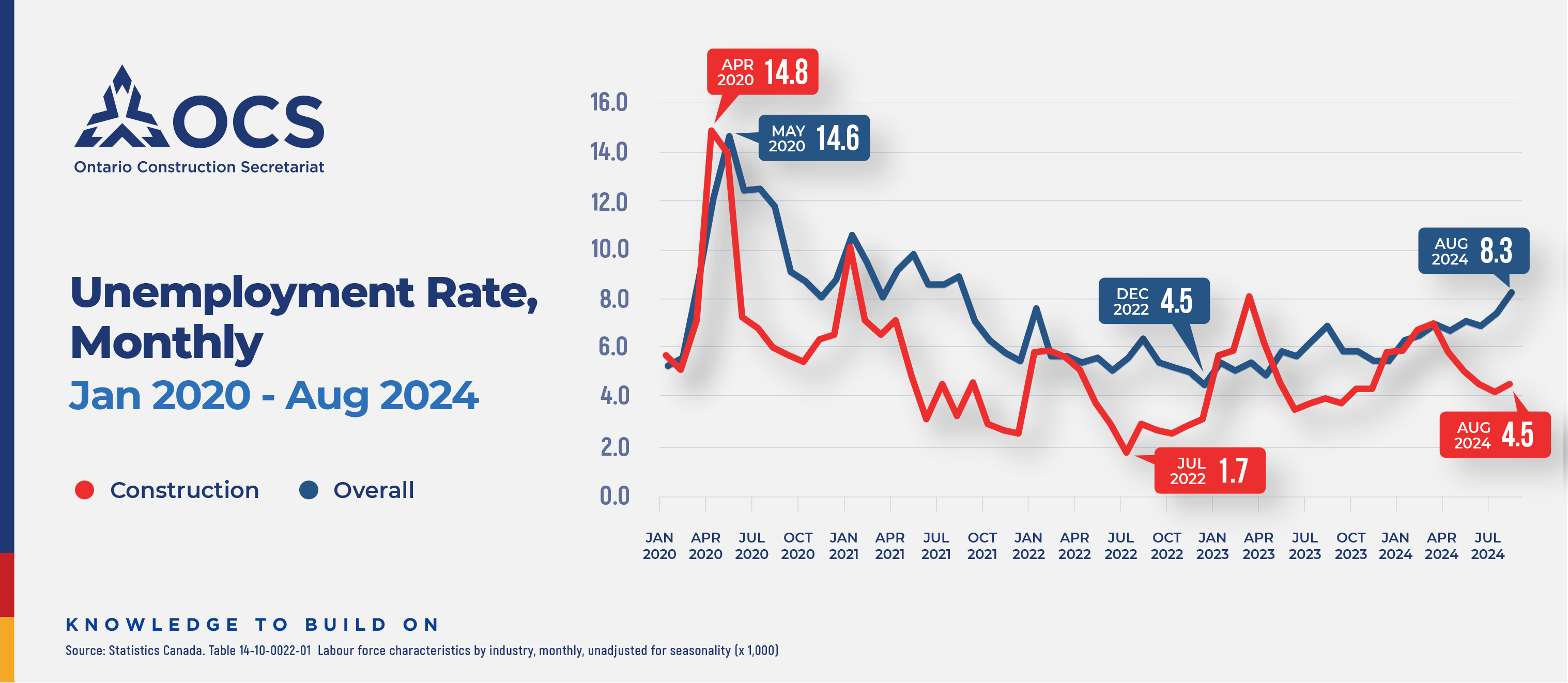

At the onset of the pandemic, unemployment surged amid new work restrictions for health and safety. Ontario’s overall unemployment rate rose to 14.6% (May 2020) and the construction unemployment rate shot up to 14.8% (April 2020). The Ontario rate took over 2 years to return to the pre-pandemic level, reaching 5.6% in 2022, and bottoming out at 4.5% in December. In contrast, the construction unemployment rate dropped down to 5.4% as early as October 2020, and by 2021 the annual average rate was actually lower than in 2019. This further dropped in 2022 to a historic low of 3.7%, reaching as low as 1.7% in July of that year. Part of the resilience of this sector came from fewer restrictions relative to other sectors, and part of it was due to strong demand (see highlight box).

Looking at the difference between the lowest and highest employment numbers throughout this 2-year period also showed a stronger bounce back in construction. Ontario saw a trough-to-peak difference of 24.8% (6.3M in April 2020 to a peak of 7.86M in June 2022), whereas in construction it was a 38.2% difference (449.2K in April 2020 to 620.6K in July 2022). Average annual employment also boomed in 2022 to 588K and again to a record breaking 596K in 2023; August 2023 was particularly noteworthy as both employment and labour force reached record highs of 624.6K and 649.9K respectively.

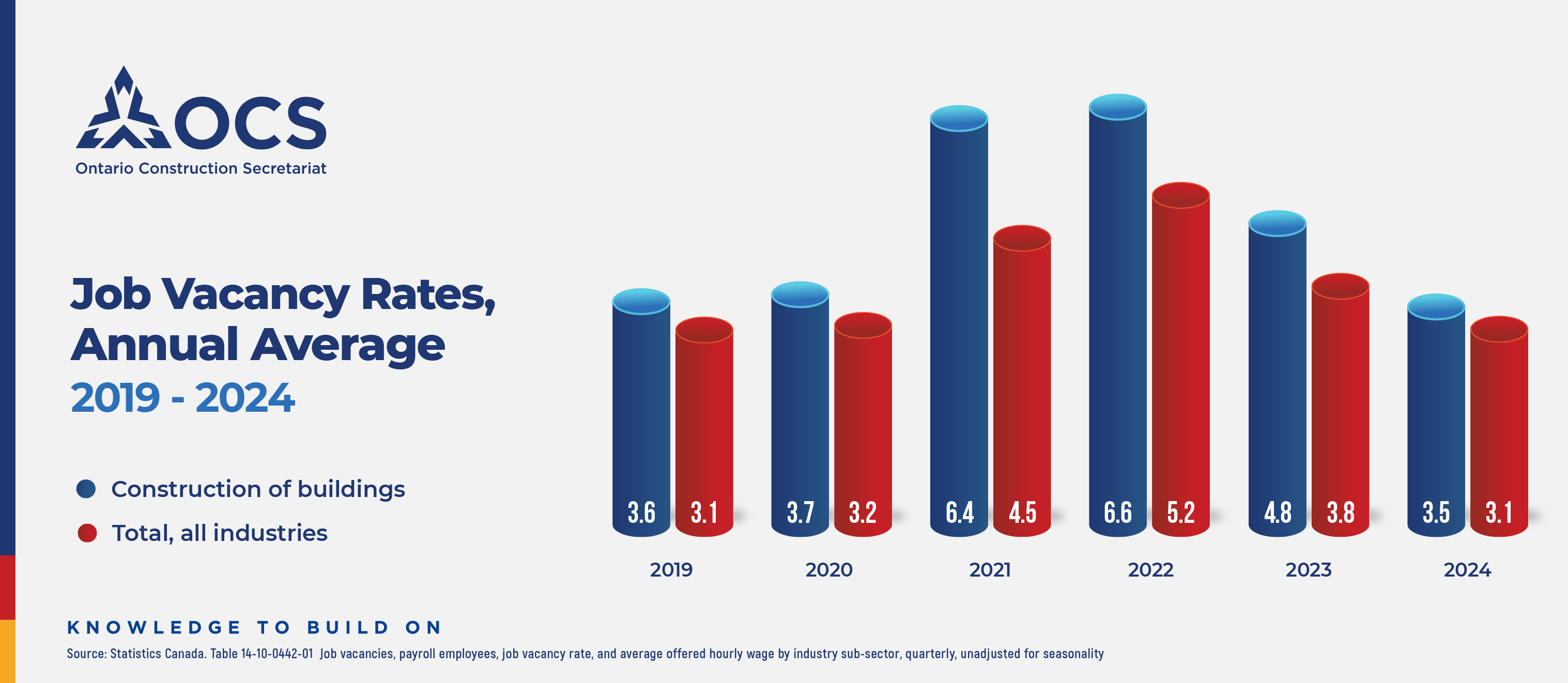

Strained Labour Markets and High Job Vacancy Rates

Despite the strong post-pandemic recovery, all industries also experienced elevated job vacancy rates – meaning the number of unfilled postings relative to total postings was increasing. In other words, positions were becoming harder to fill. This was especially pronounced in building construction, which in 2022 reached peak annual vacancy rate of 6.6%.

Recent Trends and Continued Labour Market Strain

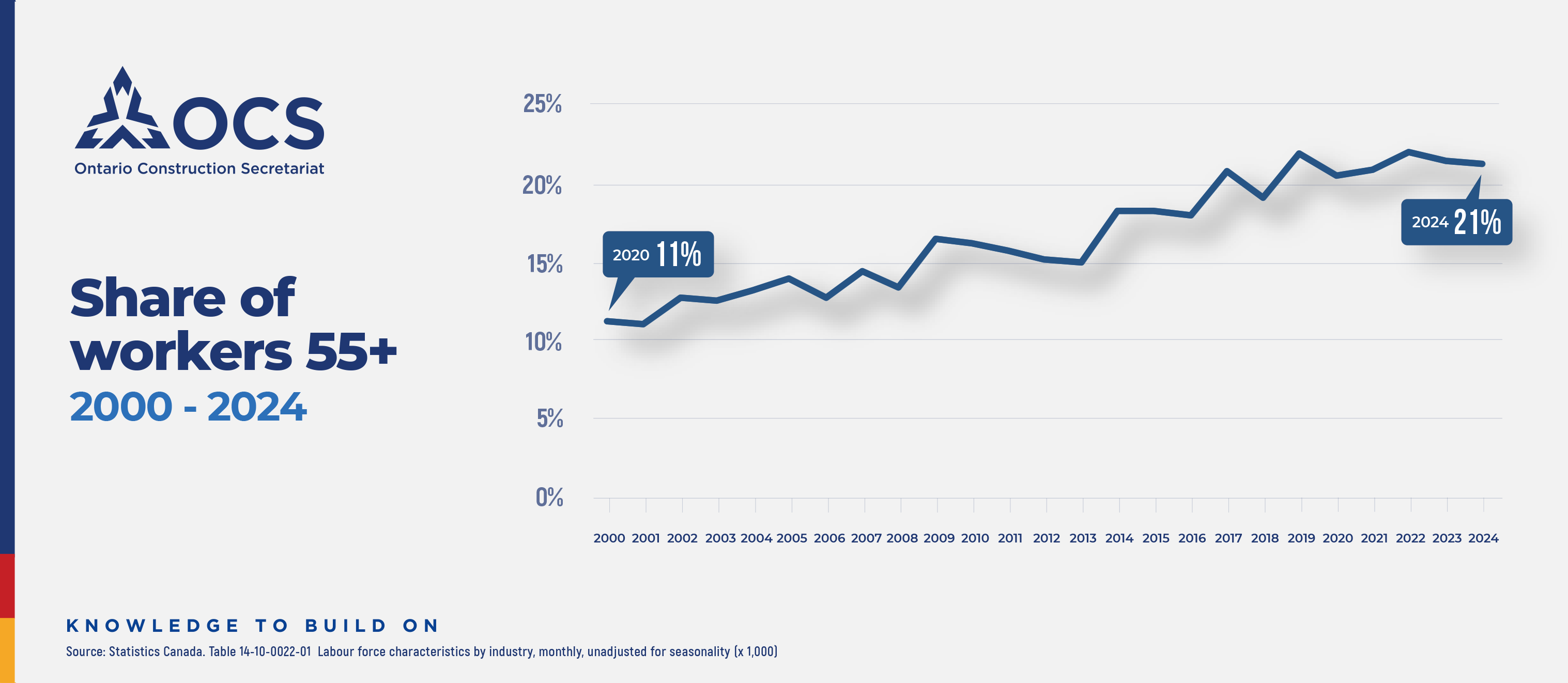

As we entered 2024, labour market conditions moderated somewhat. Employment came off the record highs and unemployment rates have been edging upwards, closer to pre-pandemic norms, as the economy cooled in the wake of interest rate hikes. Job vacancy rates also moderated to around 3%, about where they were before the pandemic. Yet labour markets are projected to remain tight in the coming years as baby-boomers continue to retire. As of 2024, the share of workers aged 55+ represents over a fifth of the construction workforce (about double the share from the early 2000s) and BuildForce Canada projected about 89,300 retirements (15.5% of the current labour force) by 2033; after accounting for the estimated increase in demand and potential new supply, a gap of about 35,500 workers will still need to be addressed.

Increasing Population and Role of Immigration

The population surge, fueled primarily through unprecedented immigration, is also adding to anticipated labour market strain through increased need for housing and infrastructure. Since 2019, Ontario population grew by 1.5 million people (+10% between Q2 2019 and Q2 2024). While adding roughly 790K to the labour force and about 640K in employment in the same time frame (+8%), the construction sector increased by a proportionally lower amount at 7% (+40K workers).

Likewise, the share of immigrants working in construction has also been proportionally lower than their share in the overall workforce. According to BuildForce, in 2023 the share of immigrants in Ontario’s construction industry was 27%, lower than the 33% share in all industries overall. The share of new immigrants intending to work in construction, as measured by new permanent residence issuances, is an even greater concern; in 2022 it was only about 2% for Ontario (CIBC Capital Markets, “If they come you will build it — Canada’s construction labour shortage”, June 2023). Evidently, increasing the share of immigrants presents an opportunity to help tilt the scales of supply and demand back in balance. The Express Entry system includes several programs to facilitate quicker immigration into Canada. These programs include Canadian Experience Class, Federal Skilled Trades Program (least utilized), Federal Skilled Worker Program, and Provincial Nominee Program (most commonly used), However, even with all these pathways, immigration has traditionally favoured those with university degrees in STEM fields (RBC Economics, “A Growing Problem: How to align Canada’s immigration with the future economy”, March 2024, and BuildForce Immigration Report, March 2024). Increasing the population without focusing on bringing in the right skills to address the need for construction further compounds pressures on infrastructure and housing. Canada’s Building Trades Union and BuildForce Canada recommend allowing more skilled trades workers into Canada through the Express Entry system with a focus on most in-demand trades and occupations. Another strategy would be to identify countries which have the skilled trades and incentivize immigration from those countries, such as by streamlining the process (RBC Economics, “A Growing Problem: How to align Canada’s immigration with the future economy”, March 3, 2024). Inter-provincial migration could also be an avenue; however, most provinces are experiencing labour market tightness (BuildForce Ontario Highlights 2024) and would therefore be in competition for workers.

Women in Construction

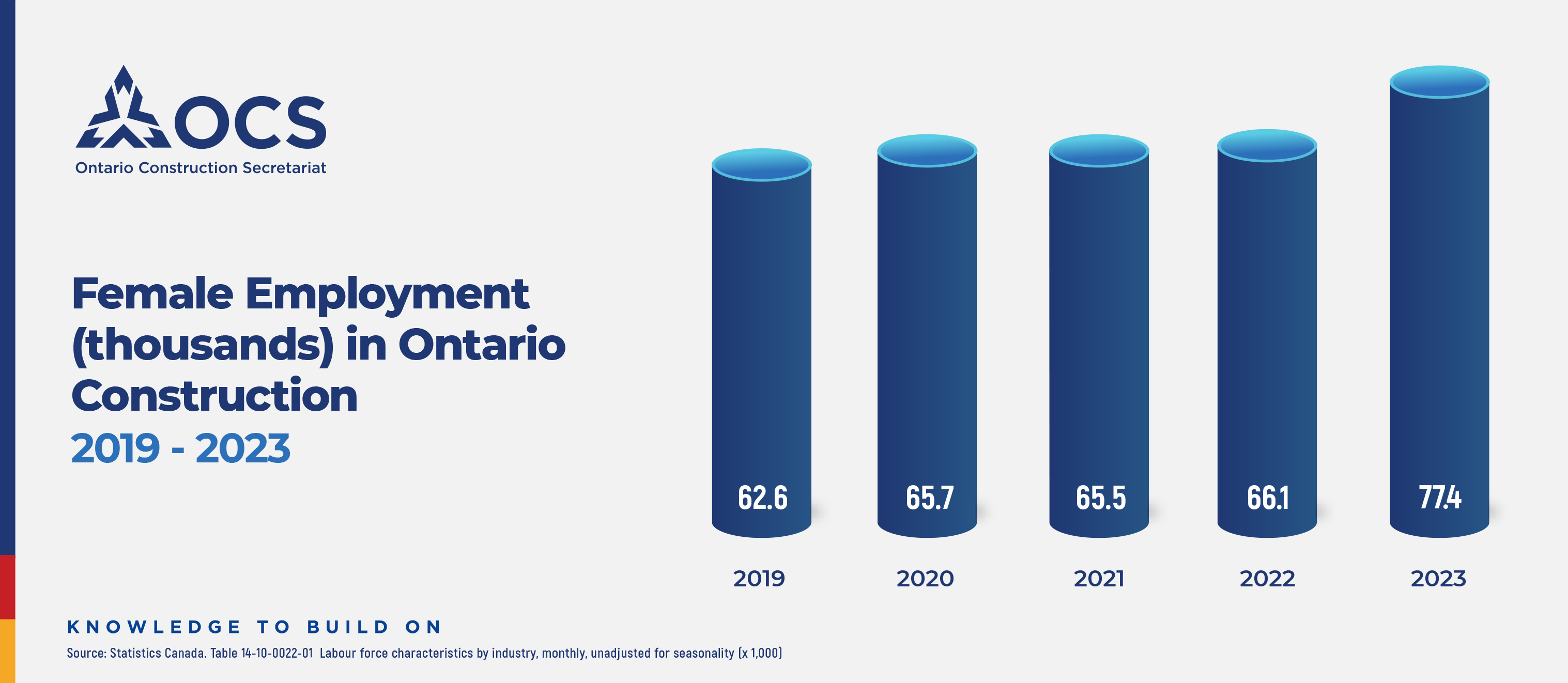

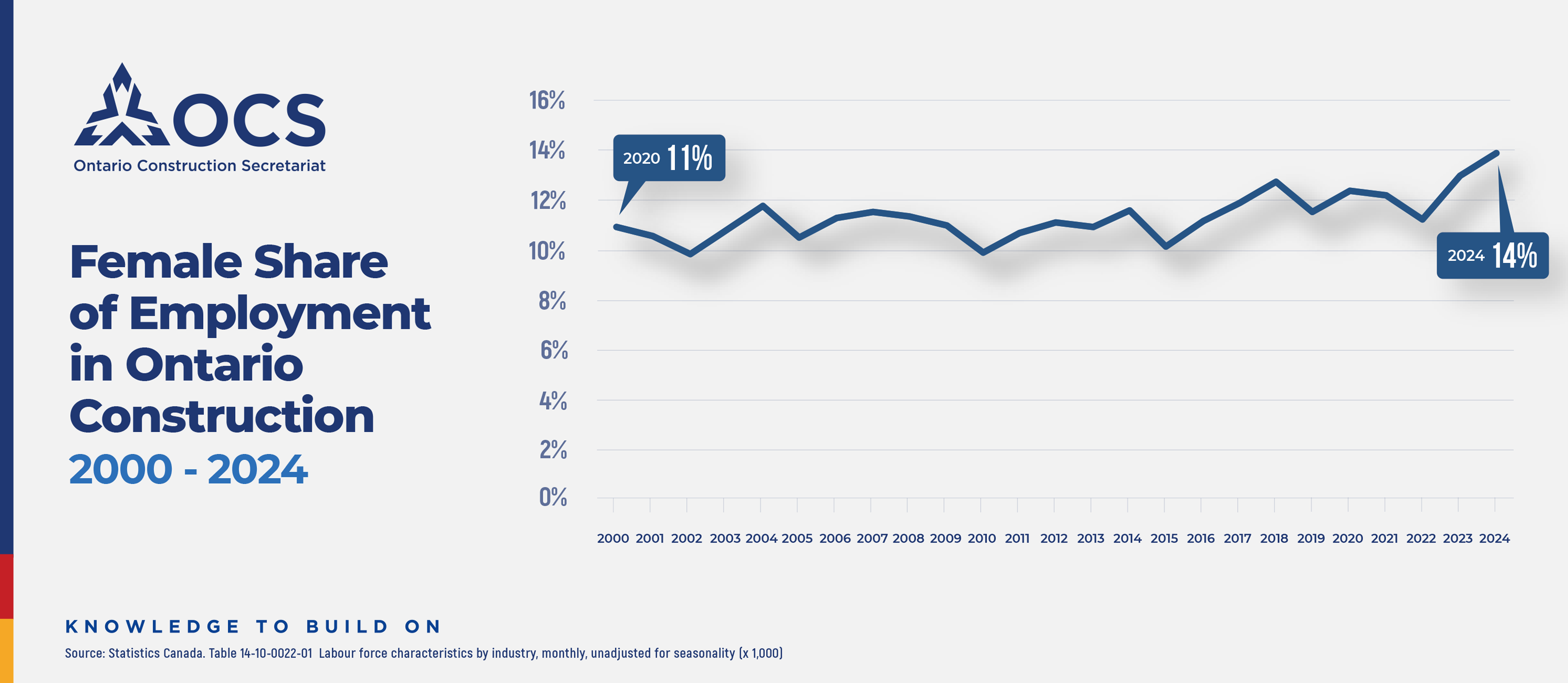

Another pathway to boosting the construction workforce would be to increase the share of underrepresented populations. Inroads have already been made on expanding female employment in construction. Since 2019, the number of females (15 and over) has been steadily increasing and saw substantial gains in 2022 and 2023. The annual average increased from 63K in 2019 to 77K in 2023, a 22% increase. This trend continued into the first half of 2024, with March recording an all-time high of 86K (36.5% higher than the 2019 average). Over the long-term, the share of females also increased, from about 11% in the early 2000s to its current share of 14%. While this is moving in the right direction, it could stand to increase further.

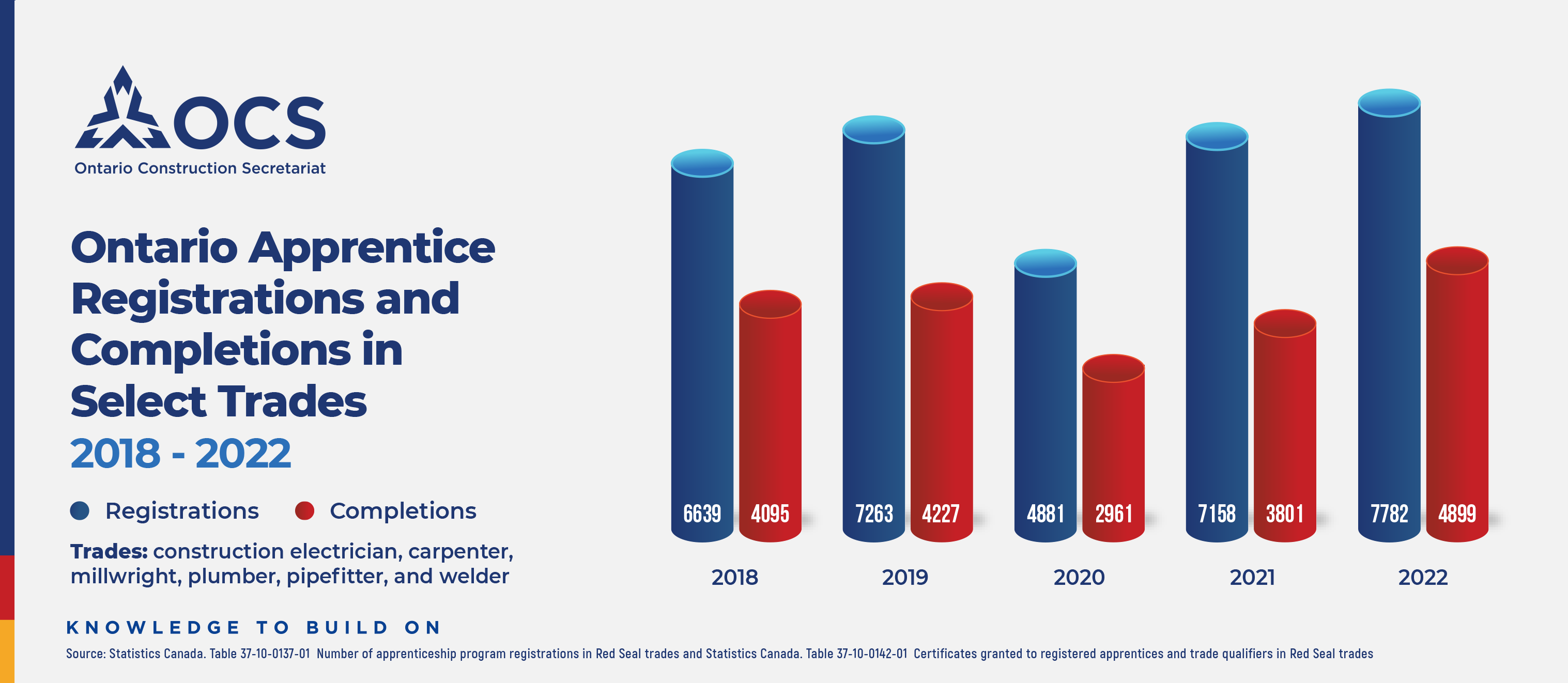

Apprenticeship Recovery

During the pandemic, students were unable to progress in their apprenticeship programs due to work interruptions. Both registrations and completions in the top Red Seal construction trades recovered in 2021 as restrictions eased. This momentum continued into 2022, as new registrations in 6 of 7 top construction related Red Seal trades (construction electrician, carpenter, millwright, plumber, pipefitter, and welder) were up 9% from 2021 and up 7% from 2019. The rebound in completions was even more pronounced. In 2022, apprentice completions in the same six construction related trades increased 29% from 2021 and 16% from 2019. The boost in certificates was mainly due to millwright and construction electrician completions (Canadian Apprenticeship Forum, Apprenticeship Registration Trends and Completion Rates, 2024). Continuing these trends will be important to offset retirements and engaging youth will be key to ensuring a healthy workforce for the future.

Conclusion

Strong construction investment has fueled historically high levels of construction employment but has also created strained labour market conditions. Although we have seen some relief in 2024, the industry needs to remain focused on attracting new workers to construction. The number of women and their historic share in the construction workforce has increased substantially. Apprenticeship has recovered from prior lows and continues an upward trend. However, the industry is still an aging, male dominated industry. Increasing the share of women and other underrepresented populations, continuing to promote apprenticeship, and ensuring Canada’s immigration policies support the construction industry are key pillars to ensuring a vibrant labour market for the future.

_____________________________

FOR MORE INFORMATION, CONTACT:

Ali Ahmad

Research Analyst

Ontario Construction Secretariat (OCS)

180 Attwell Drive, Suite 360, Toronto, ON M9W 6A9

P 416.620.5210 ext. 222

aahmad@iciconstruction.com