March 20, 2026

SUMMARY

Ontario’s construction labour market is showing signs of moderation. While employment has remained relatively stable, job vacancy rates have declined to decade lows, indicating softer hiring demand, particularly in residential construction. At the same time, the labour force has contracted, driven by declines among younger and older workers and broader population trends, including negative interprovincial migration. Growth in non-residential construction, supported by infrastructure investments, is expected to provide some stability in the near term.

LABOUR SUPPLY AND POPULATION TRENDS

The unemployment rate in Ontario’s construction sector fell to 6.7% in February, down from 7.1% in January, with approximately 2,700 more people employed compared to the previous month. However, employment remains 2.4% lower than a year ago. Despite this, the unemployment rate is lower than the same time last year, largely due to a contraction in the labour force, which declined by 3.3% year-over-year (approximately 19,800 workers).

This decline has not been evenly distributed across age groups. Year-over-year changes show a significant reduction in youth participation (15–24), which fell by 21,600, along with a decline of 16,600 among workers aged 55 and over. In contrast, the core working-age group (25–54) increased by 18,300. While this growth has helped offset some losses, it has not been sufficient to fully counterbalance declines in other age groups.

Population trends provide additional context. Ontario’s population declined 0.3% from October 2025 to January 2026, while interprovincial migration remained negative, with a net loss of 1,598 people in Q4 2025. Immigration continues to support labour supply, with Ontario receiving 42.3% (35,159) of all new immigrants to Canada during this period.

LABOUR DEMAND

Employment levels in Ontario’s construction sector have remained relatively stable; however, demand for new workers has softened. The job vacancy rate stood at 1.6% in Q4 2025, the lowest level in over a decade, with both vacancies and vacancy rates declining steadily since early 2022. This points to a more cautious hiring environment.

The slowdown is most evident in residential construction, reflecting factors such as affordability challenges, rising construction costs, and slower absorption of new housing supply. In contrast, non-residential construction is expected to remain more stable, supported by ongoing and planned investments in infrastructure and institutional projects.

SECTOR BREAKDOWN

Ontario’s construction industry comprises three main subsectors:

- Construction of buildings: new developments, additions, and repairs

- Heavy and civil engineering: infrastructure projects

- Specialty trade contractors: electrical work, masonry, painting, and other trades

In Q4 2025, specialty trade contractors employed 66.5% of construction workers, followed by construction of buildings (24.2%) and heavy and civil engineering (9.4%).

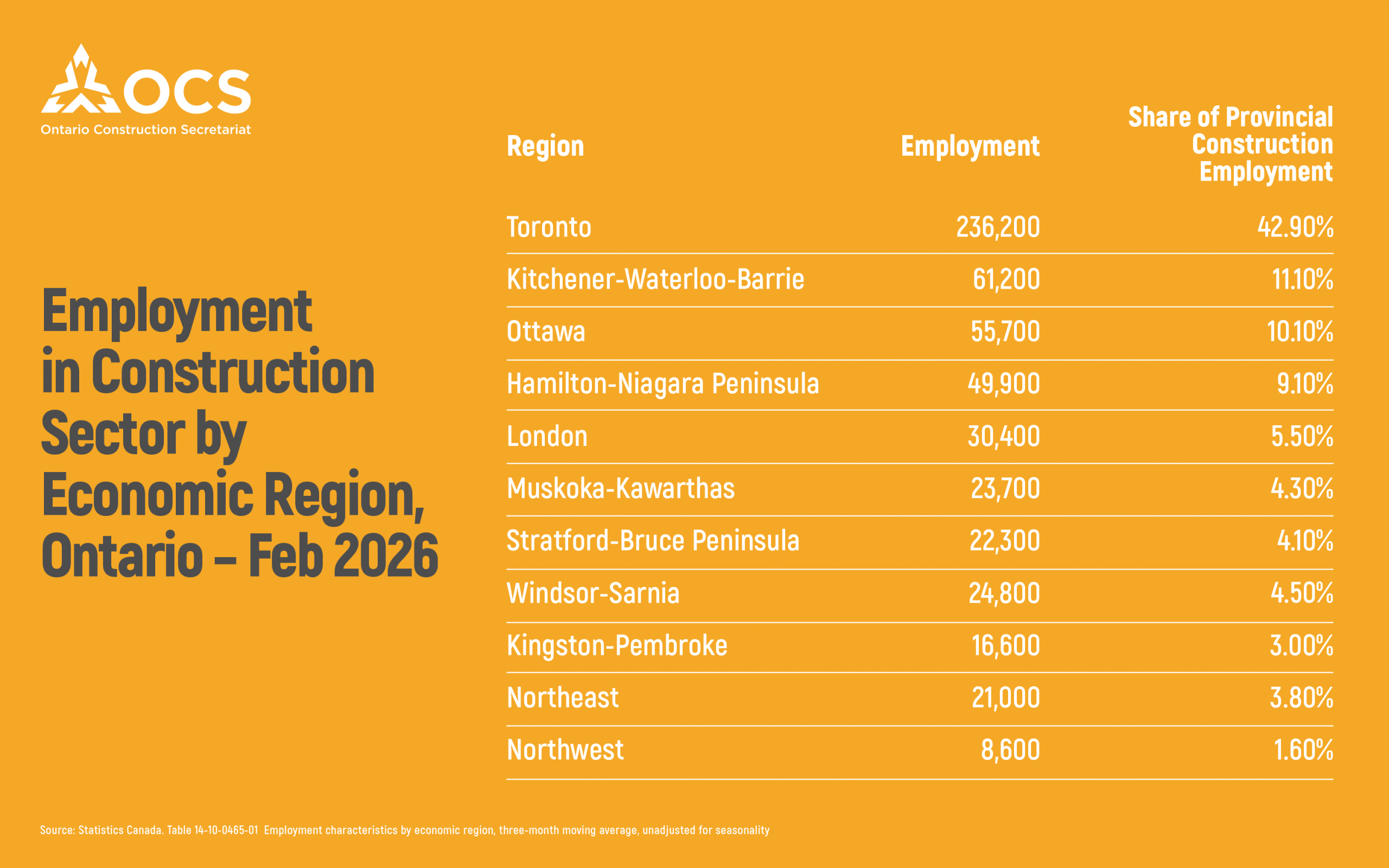

GEOGRAPHICAL DISTRIBUTION

Construction employment is concentrated in urban centres: Toronto leads with 236,200 workers (43% of provincial total), followed by Kitchener-Waterloo-Barrie (11%) and Ottawa (10%).

While employment is concentrated in larger regions, construction represents a larger share of total employment in smaller regions such as Stratford-Bruce Peninsula (12.8%) and Muskoka-Kawarthas (11.7%).

OUTLOOK

According to Job Bank Canada, non-residential construction is projected to grow through 2029, peaking around 2027. Key drivers include mining, nuclear, public infrastructure, and industrial, commercial, and institutional construction. Projects like small modular reactors at the Darlington Nuclear Station are expected to generate significant employment.

Trade uncertainties and tariffs may affect some industrial projects. Many project schedules are being adjusted given current geopolitical uncertainties, and while Ontario has a strong pipeline of work, especially in the public sector, the timing and scheduling of projects is in flux, making it difficult to assess labour market needs. Overall, the sector is positioned for moderate growth in the coming years.

Whereas, residential construction eased in 2025 due to cost pressures and excess inventory, moderate growth is expected in 2026, supported by delayed demand, though interest rate uncertainty and slower immigration may affect momentum.

____________________________

FOR MORE INFORMATION, CONTACT:

Gargi Bharti

Economic and Research Project Lead

Ontario Construction Secretariat (OCS)

180 Attwell Drive, Suite 360, Toronto, ON M9W 6A9

P 416.620.5210

gbharti@iciconstruction.com